Getting approved for a loan when you have bad credit can feel like an uphill battle—especially when you don’t have collateral to secure the loan. Traditional lenders often see bad credit as a high-risk factor, and without assets to back up the loan, the challenge becomes even greater. However, the good news is that it’s entirely possible to get approved for a bad credit loan with no collateral if you understand how the system works and take the right steps.

In this comprehensive guide, you’ll learn proven strategies, insider tips, and practical steps to improve your chances of approval—even with a low credit score.

Understanding Bad Credit and Unsecured Loans

Before diving into strategies, it’s important to understand what you’re dealing with.

What Is Bad Credit?

Bad credit typically refers to a low credit score, often below 580 on most scoring models. It usually results from:

- Missed or late payments

- High credit utilization

- Defaults or charge-offs

- Bankruptcy or collections

Lenders use your credit score to assess risk. The lower your score, the riskier you appear.

What Is a No-Collateral Loan?

A no-collateral loan—also known as an unsecured loan—does not require you to pledge any asset (like a house or car). Instead, lenders rely on:

- Your creditworthiness

- Your income

- Your financial behavior

Because these loans are riskier for lenders, they often come with:

- Higher interest rates

- Lower borrowing limits

- Stricter approval criteria

Why Approval Is Still Possible

Even with bad credit and no collateral, lenders may still approve your application because:

- Alternative lenders focus on income, not just credit

- Technology allows better risk assessment

- Demand for personal loans has increased competition among lenders

This means you have more opportunities today than ever before.

Step-by-Step Guide to Getting Approved

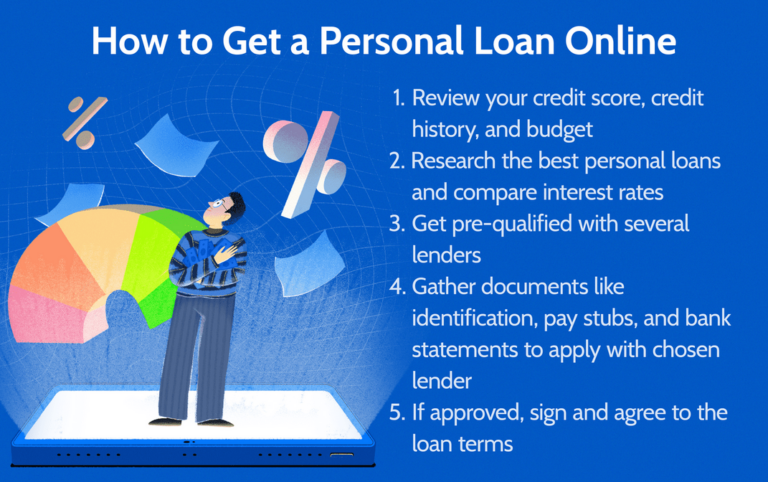

1. Check and Understand Your Credit Report

Start by reviewing your credit report. Look for:

- Errors or inaccuracies

- Fraudulent accounts

- Outdated negative items

Disputing errors can quickly improve your score.

Pro Tip: Even a small increase in your credit score can significantly improve your approval chances.

2. Improve Your Credit Score (Even Slightly)

You don’t need perfect credit—just a better version of your current score.

Quick ways to boost your score:

- Pay down credit card balances

- Make all payments on time

- Avoid opening new credit accounts unnecessarily

- Become an authorized user on a trusted account

Even a 20–50 point increase can make a difference.

3. Show Stable Income

For unsecured loans, income matters more than assets.

Lenders want to see:

- Consistent monthly income

- Stable employment or business revenue

- Ability to repay the loan

Prepare documents such as:

- Pay stubs

- Bank statements

- Tax returns (for self-employed individuals)

4. Reduce Your Debt-to-Income Ratio (DTI)

Your debt-to-income ratio shows how much of your income goes toward paying debts.

Formula:

Total monthly debt ÷ Monthly income = DTI

Lower DTI = Better approval chances.

Aim for:

- Below 40% (ideal)

- Below 50% (acceptable for some lenders)

To improve your DTI:

- Pay off small debts

- Increase income if possible

5. Apply with the Right Lenders

Not all lenders are the same. Traditional banks may reject you, but others specialize in bad credit loans.

Look for:

- Online lenders

- Credit unions

- Peer-to-peer lending platforms

These lenders often consider:

- Income

- Employment stability

- Banking history

instead of just your credit score.

6. Prequalify Before Applying

Many lenders offer prequalification tools.

Benefits:

- No impact on your credit score

- See potential loan terms

- Compare multiple offers

This helps you avoid unnecessary hard inquiries that can lower your score.

7. Consider a Co-Signer

A co-signer is someone with good credit who agrees to take responsibility if you default.

Benefits:

- Higher approval chances

- Lower interest rates

- Better loan terms

However, this is a serious commitment. Make sure both parties understand the risks.

8. Opt for Smaller Loan Amounts

The larger the loan, the higher the risk for lenders.

If possible:

- Request only what you need

- Start with a smaller loan

This increases your chances of approval and reduces financial pressure.

9. Provide Complete and Accurate Information

Incomplete or incorrect applications are often rejected.

Make sure to:

- Double-check all details

- Provide accurate income figures

- Submit required documents promptly

Honesty builds trust with lenders.

10. Demonstrate Financial Responsibility

Even with bad credit, you can show positive financial behavior:

- Maintain a steady bank balance

- Avoid overdrafts

- Show consistent deposits

Some lenders review your banking activity to assess risk.

Best Types of No-Collateral Loans for Bad Credit

Here are some options to consider:

1. Personal Installment Loans

- Fixed monthly payments

- Predictable repayment schedule

- Available from online lenders

2. Payday Alternative Loans (PALs)

Offered by credit unions, these loans:

- Have lower interest rates than payday loans

- Offer safer borrowing options

3. Peer-to-Peer Loans

Platforms connect borrowers with individual investors.

Benefits:

- Flexible criteria

- Competitive rates (depending on profile)

Common Mistakes to Avoid

1. Applying to Too Many Lenders at Once

Multiple applications can:

- Lower your credit score

- Signal desperation to lenders

2. Ignoring Loan Terms

Always check:

- Interest rates (APR)

- Fees

- Repayment period

A loan approval is not helpful if the terms are unaffordable.

3. Falling for Scams

Be cautious of:

- Guaranteed approvals

- Upfront fees

- No credit check promises

Legitimate lenders always assess risk.

4. Borrowing More Than You Can Repay

Overborrowing can lead to:

- Debt cycles

- Further credit damage

- Financial stress

Only borrow what you can realistically repay.

How to Increase Approval Odds Fast

If you need a loan urgently, focus on these quick wins:

- Correct errors on your credit report

- Pay off small debts immediately

- Show proof of steady income

- Apply with lenders specializing in bad credit

- Use a co-signer if available

Building Credit After Getting Approved

Getting the loan is just the beginning. Use it to rebuild your credit.

Best practices:

- Make all payments on time

- Set up automatic payments

- Avoid missing due dates

- Keep balances low

Over time, this can significantly improve your credit profile.

Alternative Options If You’re Denied

If you’re not approved, don’t panic. Consider these alternatives:

1. Credit Builder Loans

Designed specifically to improve credit.

2. Secured Credit Cards

Require a deposit but help rebuild credit history.

3. Borrowing from Friends or Family

Can be a temporary solution—but treat it professionally.

Final Thoughts

Getting approved for a bad credit loan with no collateral isn’t impossible—it just requires strategy, preparation, and smart decision-making.

Focus on:

- Improving your credit profile

- Demonstrating stable income

- Choosing the right lenders

- Borrowing responsibly

With the right approach, you can not only secure a loan but also take the first step toward financial recovery and long-term stability.